As the yearly transfer pricing audit wave was recently released by the Belgian tax authorities, in which Belgian taxpayers receive a (mostly) standardized, extensive request for information, it is a good moment to have a look at some recent developments as well as certain facts and figures linked to transfer pricing audits.

During a recent publication of written questions and replies of the Belgian Chamber of Representatives (dd. 16 December 2021) and a debate in the Commission for Finance and Budget (dd. 10 February 2021), the Belgian minister of finance confirmed that the Belgian tax authorities are closely monitoring the OECD’s developments regarding transfer pricing and are examining whether the regulatory framework needs to be adapted or strengthened in this respect. Reference was made to the circular letter of February 2020 in which the administration’s position is clarified (see also our previous post) and the OECD’s Pillar 1 and Pillar 2 projects.

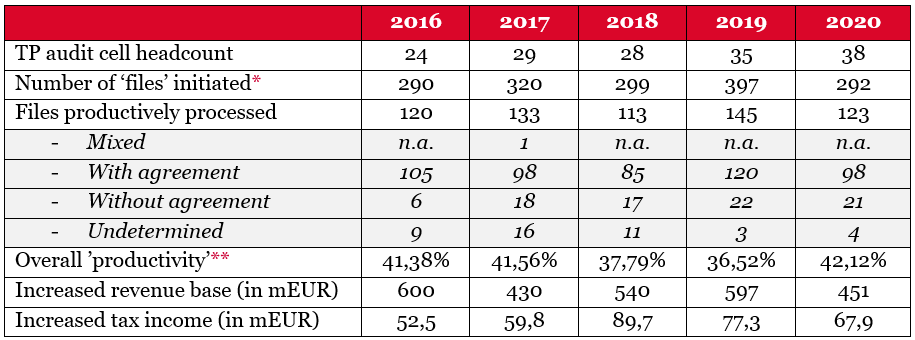

While the minister stressed that - because of the complexity of transfer pricing - quality is more important than quantity, certain evolutions of figures regarding the transfer pricing audit team in Belgium were provided. The figures are included in the below table.

* We note that the answer of the finance minister is not fully clear on how many audits were undertaken by the TP audit cell. In his response, reference is made to the number of assessment years that have been audited, whereas an audit is often carried out / has an outcome for multiple assessment years. A formal ‘file’ (borderel/bordereu de donnees) is created for each assessment year in the year the audit is initiated, irrespective of whether the audit was labelled productive.

** We note that ‘productivity’ is computed as ’files productively processed’ divided by the ’number of audits that were initiated’ and does not represent the success rate interpreted as an audit that was concluded with(out) an adjustment.

The Belgian minister of finance confirmed that in general, auditors are granted a period of 18 months to perform the transfer pricing audit.

Whereas these numbers mainly show that there has been an increased focus on transfer pricing from the specialized transfer pricing audit cell over the years (except for 2020 for which numbers are impacted by delays due to the covid-19 pandemic), these numbers do not tell the full story.

In practice, we have seen that data mining techniques used to select target companies have been improving, leading to a better audit selection process. Nevertheless, there is room for further improvement as information that is included by taxpayers in local file forms (275.LF) and master file forms (275.MF) (for taxpayers that exceed the relevant thresholds) is not yet fully assessed in detail prior to an audit being initiated / audit selections are being made. This results in an additional administrative burden for taxpayers and should be further improved.

Another important evolution is that, next to the specialized transfer pricing audit cell, also other teams are focusing more and more on transfer pricing related topics, for which the actual figures are not included in the above table. We notice that the respective Large Companies teams as well as the Special Investigation Squad (BBI/ISI) are auditing transfer pricing topics. In some cases, they may be supported by the specialized transfer pricing audit cell. In practice, different teams are unfortunately not always aware of other audits procedures / transfer pricing topics that may have already been covered in another audit. Information sharing within the various teams could be improved in this respect, as taxpayers should not be audited on the same topic for the same tax years a second time. Therefore, such cases should be flagged immediately to the audit team in order to avoid administrative burdens for taxpayers and tax inspectors.

The number TP auditors has increased over time. In the budget, it was announced that the capacity of the TP audit team would be doubled. Today, the Belgian tax administration is searching for 25 additional employees in transfer pricing and international tax to strengthen the team. They are explicitly searching for people with a thorough knowledge of international taxation, and more in particular in transfer pricing, double taxation treaties and the European directives related to corporate taxation.

As transfer pricing audits are here to stay, being prepared for an audit as well as knowing how to handle a lengthy audit procedure are important for companies. We can assist you with both. We, as economists of Tiberghien economics, can work together with tax lawyers of Tiberghien lawyers as one multidisciplinary team having vast experience in dealing with tax and/or transfer pricing audits. Our team consists of highly experienced people with in-depth knowledge in the domains of tax, transfer pricing and procedural aspects including litigation.

For further information, please contact the authors if this article or have a look at the broad level of information and tips included on our website https://www.tpaudit.com/.

Ben Plessers – Senior Manager at Tiberghien economics (ben.plessers@tiberghien.com)

Heleen Van Baelen – Senior Manager at Tiberghien economics (heleen.vanbaelen@tiberghien.com