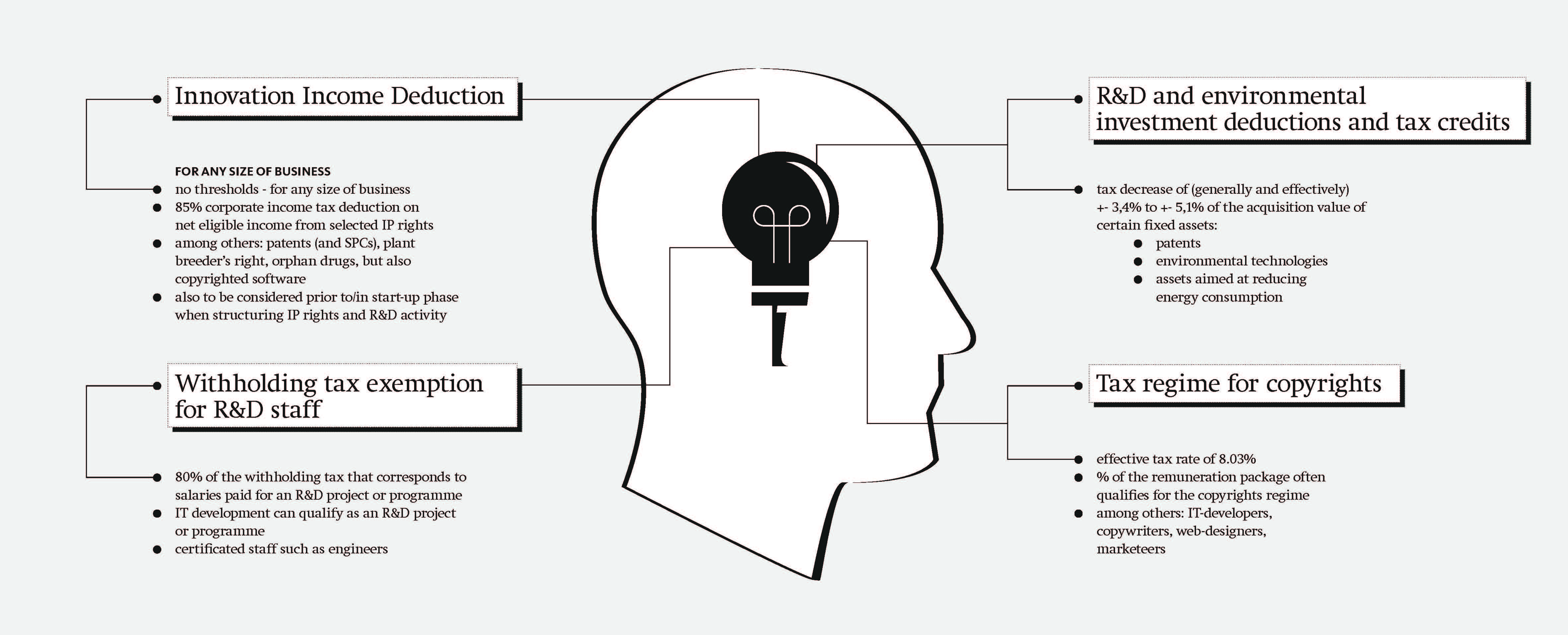

The patent income deduction (“PID”)/innovation income deduction (“IID”) is a fiscal incentive to promote research and development activities in Belgium. Companies that innovate can, based on this fiscal regime, exempt 80% (PID)/85% (IID) on the qualifying income from their taxable base. As a result of the BEPS-action plan, the PID will phase out in June 30, 2021 and has been replaced with the IID.

In 2019, 124 requests for an advance decision with respect to the application of the PID/IID have been made compared to 103 in 2018. Of the 107 decisions that have been granted (versus 91 in 2018), 56 have been applied for by large companies and 51 by SMEs. We note that the decrease in the number of applications is mainly due to the increase in applications made by SMEs (from 38 to 51 applications).

In the annual report, reference is also made to an additional agreement (“avenant”)to an already granted decision. This decision relates to the application of the PID with respect to license income received for 3 patents that were obtained that were required to produce a specific material. A first avenant related to this decision was granted in 2017. This avenant related to the development of a new application based on the same 3 patents. A second avenant has been granted by the SAD and relates to an application of a patent applied for by the end of 2018. The SAD takes the position that as long as the additional patent has not been granted, the PID can still be applied as the additional patent applied for could be considered as an improvement of the older patents for which the PID is applied (as long as no exempted reserve in application of the IID is made in line with art. 194 quinquies WIB92). The decision states that in the taxable year in which the patent will be obtained, the income related to this additional patent can no longer benefit from the transition regime and as such the IID should be applied. This means that a split should be made of the income for which the PID will be applied and the income for which the IID will be applied and this until June 30 2021 (the moment at which the transition regimes ceases to exist). Given the complexity of the transition from the PID to the IID, a profound analysis of the patents that were obtained or were applied for per product is highly recommended.

With respect to innovative copyright protected software we note that rulings are only granted by the SAD for a 3-year period and that this also applies for other rulings including a benchmark analysis. In this respect, he SAD refers to the Circular Letter issued on February 25 2020 regarding transfer pricing (2020/C/35) stating that a benchmark analysis should preferably be performed every 3 years, unless the facts and circumstances require an earlier review.

Finally, we note that the decisions granted by the SAD on the IID for software are only valid insofar a positive advice regarding the innovative character of the software is granted by BELSPO.

Determine the embedded royalty

To determine an embedded royalty, a combination of several analyses is advisable such as:

For software, the SAD provided for a methodology to determine the IID in its 2018 annual report. More specifically, this methodology can be applied for software companies that provide licenses to their clients.

In practice, we noted that the rule of thumb is applied by the SAD on the outcome resulting from the above analyses. The underlying rationale of the SAD is that a third party licensee would not be prepared to “give away” all profit he can realize above the routine profit of the sector in which he is operating to a potential licensor.

Attention points

Discussions on the application of the IID for software typically relate to the legal ownership of the developed software and whether it is clear as from the start of a project and contract concluded with the client who the legal owner is of the developed software. It is therefore highly recommended to clearly stipulate the legal owner of the software and this as from the start of a project.

Also the calculation of the gross innovation income is an attention point i.e., license fees received from clients using software typically also include start-up costs, training, etc. which cannot be considered gross innovation income.

We also note that intellectual property that has been partially or fully developed by a company and of which the R&D costs are not recorded as an asset in the annual accounts, cannot be considered an intangible and consequently, the amount that would be received in case the intellectual property is sold can as such not be qualified as innovation income to be eligible for the IID.

Finally, the Circular Letter/C/95 FAQ recently issued provides more guidance on the application of the IID.

For any questions, please reach out to our specialists: Tine